When you pick up a prescription, you might assume your insurance will cover it - but that’s not always true. Behind the scenes, your health plan uses something called a formulary to decide which drugs it pays for, how much you pay, and even which ones you can get at all. This isn’t just paperwork. It directly affects whether you can afford your meds, if you’ll have to switch to a different drug, or if you’ll be stuck waiting for approval just to get your treatment.

What Is an Insurance Formulary?

An insurance formulary is a list of prescription drugs that your health plan covers. It’s not random. Every drug on the list has been reviewed by doctors, pharmacists, and health economists to balance effectiveness, safety, and cost. Think of it as a curated shopping list - but instead of snacks or shoes, it’s medications.

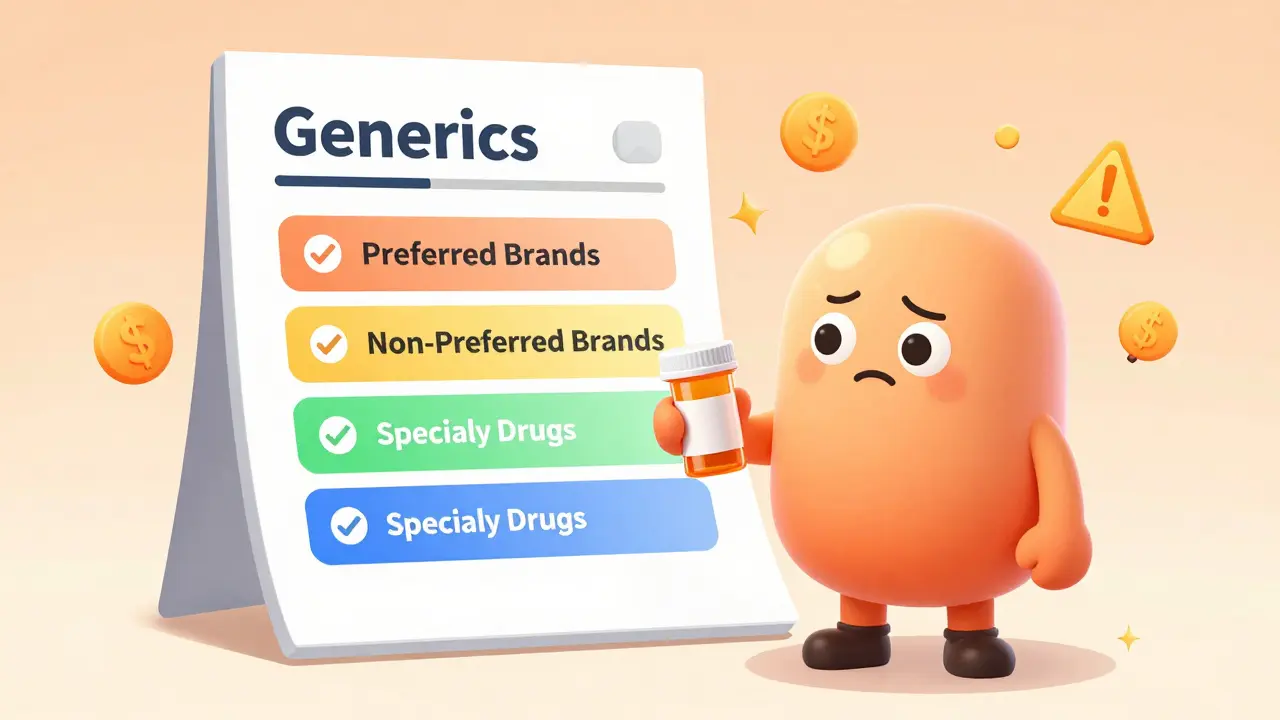

Most plans use a tiered system to organize these drugs. The typical structure has four tiers:

- Tier 1: Generics - These are the cheapest. You usually pay $10-$15 per prescription. Most formularies include at least two generic options in each common drug class.

- Tier 2: Preferred brands - These are brand-name drugs your plan favors. Copays are around $40-$50. They’ve been shown to work well and cost less than other brands.

- Tier 3: Non-preferred brands - These cost more - often $70-$100. Your plan may still cover them, but only if there’s no better alternative.

- Tier 4: Specialty drugs - These are high-cost medications, like those for cancer, MS, or rare diseases. You might pay 33% of the full price. That can mean $1,000+ a month. Some plans have no annual cap on these costs.

Switching from Tier 1 to Tier 4 can triple or even quadruple your out-of-pocket cost. A 2023 GoodRx survey found that 68% of patients experienced a formulary change that increased their drug costs - and 42% skipped doses because they couldn’t afford it.

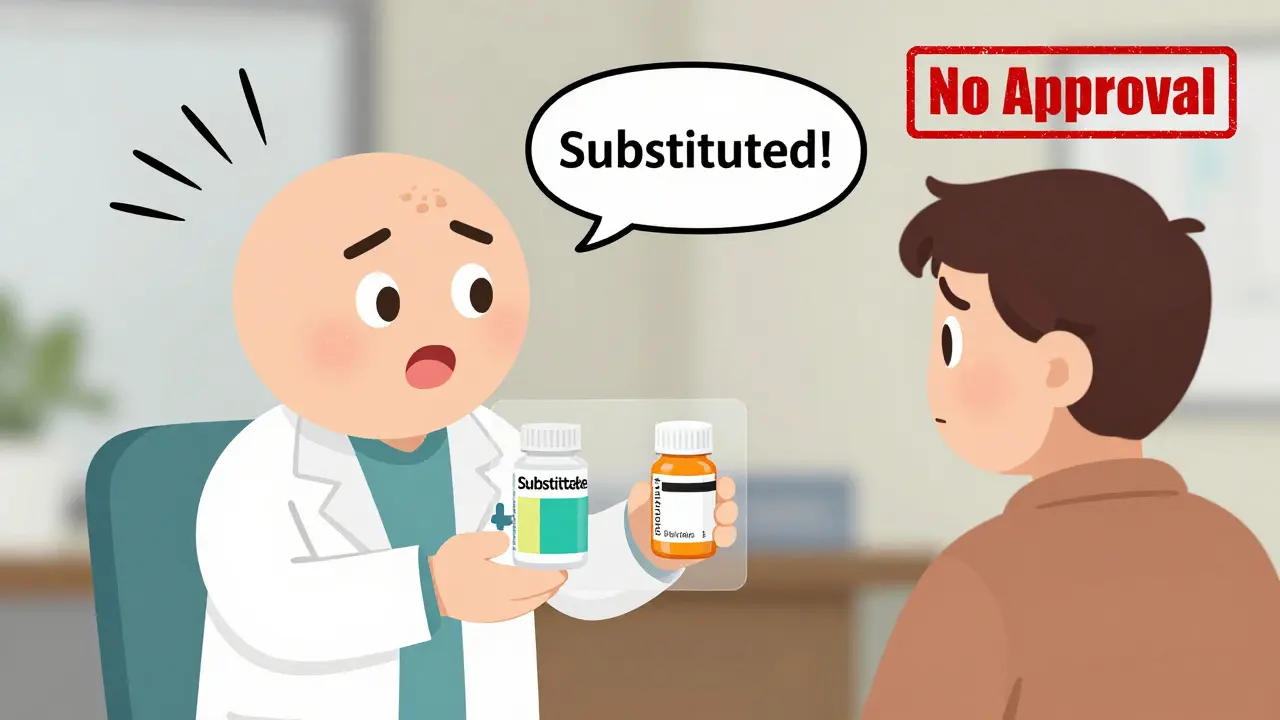

How Substitution Works - And When It Hurts

Pharmacists don’t always give you the exact drug your doctor prescribed. In 31 states, laws allow them to substitute a cheaper drug from the same therapeutic class - this is called therapeutic substitution. For example, if your doctor prescribes Humira, the pharmacist might give you a biosimilar like Amjevita, which works similarly but costs less.

This sounds like a win - and sometimes it is. But it’s not always safe or simple. A 2023 study in the American Journal of Managed Care found that 18% of prescriptions are substituted without the patient’s knowledge. For people with chronic conditions like rheumatoid arthritis or Crohn’s disease, even a small change in medication can trigger flare-ups or side effects. One Reddit user shared how their Humira was switched without warning - and their monthly cost jumped from $45 to $1,200.

Some drugs don’t have substitutes. Others, like biologics, have complex mechanisms that make substitution risky. That’s why your doctor must approve substitution in some cases - but not all. You have no way of knowing unless you ask.

Formulary Types: Open, Closed, and Everything In Between

Not all formularies are built the same. There are three main types:

- Closed formularies - Only drugs on the approved list are covered. If your med isn’t on it, you pay full price unless you get an exception. About 65% of Medicare Part D plans use this model. They keep premiums low - but restrict access.

- Open formularies - These cover almost all drugs, even ones not on the list. But you pay higher monthly premiums - usually $18-$22 more than closed plans. Only 22% of Part D plans use this.

- Partially closed - A mix. Some drugs are covered, others aren’t. This is the most common for employer-based plans.

The type of plan you have determines how much control you have. Medicare Part D plans must cover all recommended vaccines at $0 cost. But for other drugs? It’s a maze. One 2022 analysis showed the same drug could be in Tier 2 on one plan and Tier 3 on another - creating a $60 difference per prescription.

Access Restrictions: Prior Auth, Step Therapy, and Quantity Limits

Even if your drug is on the formulary, you might still face roadblocks:

- Prior Authorization - Your doctor has to prove to the insurer why you need this drug. The American Medical Association reports 82% of physicians experience delays. In 34% of cases, these delays caused serious harm - like missed cancer treatments or hospitalizations.

- Step Therapy - You must try and fail on cheaper drugs first. For example, if you have depression, your plan might force you to try two generic SSRIs before approving Lexapro. This can take weeks. For someone in crisis, that’s dangerous.

- Quantity Limits - You can only get a 30-day supply when your doctor ordered 90. Or you can’t refill early. This forces patients to juggle refills, miss doses, or pay out of pocket.

These rules exist to save money - but they often save it at the patient’s expense. A 2024 CMS audit found that 43% of formulary changes happen without any notice. You might wake up one day to find your drug gone - and your copay doubled.

How to Protect Yourself

You can’t control your insurer’s decisions - but you can control how you respond. Here’s what to do:

- Review your formulary every year - During open enrollment (October 15-December 7 for Medicare, November 1-January 15 for ACA plans), check every medication you take. Use your plan’s online tool. Don’t trust your memory.

- Know your tier - If your drug is in Tier 3 or 4, consider switching plans. A 2023 Patient Advocate Foundation study found that people who checked tiers before choosing a plan saved an average of $1,200 a year.

- Ask about exceptions - If your drug is denied, your doctor can file an exception. CMS data shows 73.2% of these requests are approved. But you have 72 hours to submit documentation. Don’t wait.

- Use tools like Medicare Plan Finder - It processes over 1.2 million searches monthly during enrollment. People who compare at least three plans save an average of $472 annually.

- Ask your pharmacist - If they switch your drug, ask why. Demand to know if it’s a substitution or a formulary change.

And if you’re on insulin? Good news - since 2023, Medicare Part D caps insulin at $35 per month. That’s thanks to the Inflation Reduction Act. But for other specialty drugs? No such protection… yet.

What’s Changing in 2025 and Beyond

The rules are shifting fast. Starting January 1, 2025, Medicare Part D will cap out-of-pocket drug costs at $2,000 per year. That’s huge. It means insurers will have to restructure their formularies - possibly moving more drugs to lower tiers to avoid hitting the cap.

Also, by January 1, 2026, all Part D plans must show real-time drug costs and formulary status at the point of prescribing. That means your doctor will see your copay before they write the script. Early pilots show this reduces prior authorization requests by 28%.

Some insurers are even testing outcomes-based formularies. If your diabetes drug keeps your HbA1c under 7.0%, your copay drops. It’s a shift from paying for drugs to paying for results.

By 2030, experts predict formularies will use genetic data to personalize tiers. If your DNA shows you respond better to Drug A than Drug B, your plan might cover only Drug A - and save money while improving outcomes.

But here’s the catch: as specialty drugs become more common, the price gap between generics and brands is shrinking. In 2023, generics cost 85% less. By 2030, that gap may drop to 65%. That means formularies will have less leverage - and patients may pay more.

What You Need to Remember

Your insurance formulary isn’t just a list. It’s a gatekeeper. It decides whether you can afford your treatment, whether you’ll be switched to a different drug, and whether you’ll have to fight just to get what your doctor ordered.

Don’t wait until your prescription is denied. Review your formulary every year. Know your tier. Ask questions. Use the tools. And if you’re on a chronic medication, keep a printed copy of your formulary in your wallet. You never know when you’ll need it.

What happens if my drug is removed from the formulary?

If your drug is removed, your insurer must notify you before the change takes effect - but many don’t. You’ll likely have to pay full price unless you file an exception. Your doctor can submit a request based on medical necessity. Approval rates are high (73.2%), but the process can take up to 7 days. If you’re in urgent need, you can request an expedited review, though approval drops to 38.5%.

Can my pharmacist substitute my prescription without telling me?

Yes - in 31 states, pharmacists can legally substitute a cheaper drug in the same therapeutic class without your doctor’s approval. This is called therapeutic substitution. It’s common for generics and biosimilars. But if your drug has no safe substitute - like a biologic for autoimmune disease - you should ask your pharmacist to confirm the substitution. Always check the label and ask: "Is this the same as what my doctor prescribed?"

Why do two plans cover the same drug but charge different prices?

Because each plan negotiates separately with drug manufacturers and Pharmacy Benefit Managers (PBMs). One plan might place a drug in Tier 2 because they got a better rebate. Another might put it in Tier 3 because they didn’t. A 2022 MMIT analysis showed the same drug could cost $30-$60 more per prescription depending on the plan. That’s why comparing formularies before choosing a plan saves money.

What’s the difference between a formulary and a drug list?

There’s no difference - "formulary" and "drug list" mean the same thing. Both refer to the official list of medications your insurance plan covers. The term "formulary" is used more in professional and regulatory contexts, while "drug list" is often used in consumer materials to make it easier to understand.

Do all insurance plans have formularies?

Almost all. Medicare Part D plans are required by law to have a formulary. Most employer-sponsored plans and individual market plans (like those on Healthcare.gov) also use them. Only a few very basic or short-term plans may not. But if you’re getting prescription drug coverage, you’re almost certainly on a formulary. Check your plan documents - they’re required to provide one.

trudale hampton

Man, I wish more people knew about tiered formularies before signing up for insurance. I got stuck with a Tier 3 drug last year and didn’t realize until my copay jumped from $35 to $92. Took me three calls to my pharmacy and a letter from my doctor to get it switched. Don’t wait until you’re at the counter - check your plan every year like the post says.

Allison Priole

so like… i just found out my insulin is capped at 35 now?? i’ve been paying $120 a month for 3 years and just assumed that was just life?? like… why didnt anyone tell me this?? i feel so dumb rn. also my pharmacist switched my biologic last month and i didnt even notice till i checked the bottle. wtf. 🤦♀️

Paul Cuccurullo

It is both a tragedy and a marvel that our healthcare system has evolved into a labyrinth of formularies, tiers, and prior authorizations - each designed ostensibly to control cost, yet ultimately burdening the very individuals they claim to serve. The irony is palpable: while insurers optimize for fiscal efficiency, patients are left navigating a maze with no map, no compass, and often, no time.

One cannot help but reflect on the moral implications of a system where access to life-sustaining medication is contingent upon bureaucratic approval, financial capacity, and the whims of corporate negotiations. The 73.2% approval rate for exceptions sounds encouraging - until one realizes that nearly three in ten patients are denied care, often with dire consequences.

And yet, there is hope. The 2025 cap on out-of-pocket costs represents a seismic shift - not merely financial, but philosophical. It suggests that society may finally be moving toward the recognition that health is not a commodity, but a right. The future of outcomes-based formularies, while complex, holds promise: a system that rewards efficacy, not just expense.

Let us not mistake policy change for justice. But let us also not underestimate the power of informed patients demanding better. Knowledge, as this post so clearly demonstrates, is not merely power - it is survival.

Bryan Woody

Yup. Insurance companies are basically playing Tetris with your prescriptions. They shove the cheap stuff to the bottom, stack the expensive ones on top, and then act shocked when you can’t reach your meds. Step therapy? That’s just ‘try the cheap one first’ with extra paperwork and a side of suffering. And don’t get me started on pharmacists substituting without telling you - like, thanks for saving me $100 but also I’ve been having seizures since you switched my meds. 🙃

Pro tip: If your doctor writes ‘do not substitute’ - write it in giant letters. And bring a lawyer. Just kidding. Or am I?

Timothy Olcott

AMERICA IS GETTING ROBBED. WHY DO WE LET THESE BIG PHARMA AND INSURANCE COMPANIES DO THIS?? I PAY TAXES I PAY PREMIUMS I PAY COPIAYS AND STILL I CAN’T GET MY DRUG?? THIS IS SOCIALISM FOR CORPORATIONS. WE NEED A REVOLUTION. 🇺🇸🔥

Kyle Young

It’s fascinating how formularies function as both economic tools and moral arbiters. The tiered structure isn’t merely a cost-control mechanism - it’s a value hierarchy encoded in pharmaceutical policy. Tier 1 isn’t just cheaper; it’s deemed ‘morally acceptable’ by health economists. Tier 4 isn’t just expensive; it’s framed as ‘exceptional’ - a privilege rather than a necessity.

But what does this say about our society’s perception of health? We accept that some lives are worth more than others, based on whether their treatment fits within a negotiated rebate structure. The fact that 42% of patients skip doses due to cost isn’t a failure of individual choice - it’s a failure of collective ethics.

And yet, the emerging shift toward outcomes-based formularies suggests a potential reorientation: from paying for pills to paying for wellness. If we can measure health outcomes and tie reimbursement to them, we may finally be moving toward a system that values healing over profit. The question is - will that change reach those who need it most?

Emily Hager

While I appreciate the detailed exposition of formulary mechanics, I must express profound concern regarding the normalization of pharmaceutical rationing under the guise of fiscal responsibility. The very premise of tiered drug access is predicated upon a utilitarian calculus that implicitly devalues human life based on economic utility. One cannot help but draw parallels to historical eugenic policies that similarly categorized individuals by perceived worth.

Furthermore, the suggestion that patients should ‘review their formulary annually’ is not a solution - it is an indictment of a system that places the burden of bureaucratic navigation onto the sick. This is not empowerment; it is institutionalized exhaustion.

Until we dismantle the PBM-insurer oligopoly and establish universal, transparent, and equitable drug coverage, we are not merely managing costs - we are managing suffering.

Shameer Ahammad

Let me tell you something - in India, we don’t have this mess. My aunt takes a biologic for rheumatoid arthritis and pays $15 a month. Why? Because the government negotiates directly with manufacturers and bans patent evergreening. Here? You need a PhD to understand your insurance. I don’t understand how Americans tolerate this. You have the world’s largest economy - and you can’t fix drug pricing? This is embarrassing.

Alexander Pitt

One thing no one talks about: pharmacy benefit managers (PBMs). They’re the middlemen between insurers and drug makers. They negotiate rebates, but you never see the savings. They’re the reason the same drug costs $30 on one plan and $90 on another. They’re not regulated. They make billions. And they’re the real reason your copay keeps going up.

Google ‘PBM reform’ - it’s the real fight.

jared baker

Just check your plan every year. That’s it. No magic. No drama. Just do it. You’ll save money. I did. Done.

David Robinson

Wow. This is the most detailed thing I’ve ever read about insurance. Thanks for the 10-page essay. Can we get a TL;DR? Like… just tell me if my drug is covered or not. That’s all I care about.

Amadi Kenneth

THIS IS A GOVERNMENT COVER-UP. FORMULARIES ARE A SECRET WEAPON USED BY THE COUNCIL OF PHARMA ELITES TO CONTROL THE POPULATION. THEY USE PBMs TO TRACK YOUR DNA AND ALTER YOUR MEDS BASED ON YOUR EMOTIONS. I SAW A VIDEO ON TIKTOK WHERE A DOCTOR SAID THEY’RE TESTING DRUGS ON PEOPLE WHO USE THE SAME PHARMACY. THEY’RE USING YOUR INSURANCE INFO TO CREATE A GLOBAL CONTROL NETWORK. THEY’RE WATCHING YOU RIGHT NOW. 🕵️♂️👁️